three ways to invest in ESG

“How you do anything is how you do everything.”

How is the summit of realization.

A hatchling will realize death or life as a consequence of its ability to fly. In between its nest and Earth lives one resolution: how.

how to invest in ESG

Methods of investment lean heavily on both your objective and tolerance. ESG Investing, Socially Responsible Investing, and Impact Investing vary in their instruments of investment—the differences detailed here. The focus of this article is strictly how to align your investments within the structure of ESG Investing.

There are three root methods when contributing capital with your conscience in an ESG framework: on your own, with a robo-advisor, or with a financial planner. Each avenue births a separate set of pros and cons, and each one is better suited for a different type of person. Don’t fret… the goal of this article is not to convince all of you to hire a financial planner—though it is best for some people.

the jist

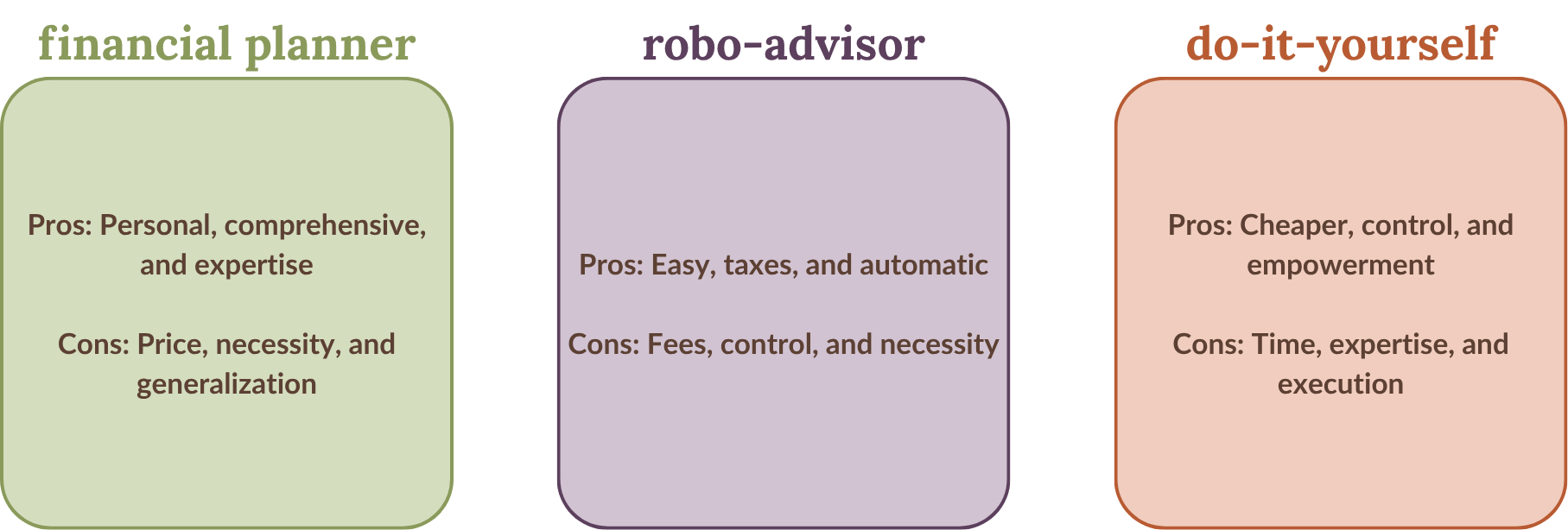

There are three main methods to align your capital and conscience as an ESG investor: do-it-yourself (DIY), robo-advisor, or financial planner. Choosing the right method for yourself focuses on different pros and cons, and evaluating which one meets your specific wants and needs best. Sometimes, the different methods can even be used in conjunction. A financial planner who doesn’t manage investments might teach you how to DIY it or point you to a robo-advisor suited for you. Below is a brief description of the pros and cons for each method.

Brief pros and cons list of using a financial planner, robo-advisor, or doing it yourself for ESG Investing.

do-it-yourself ESG investing

People are very capable of managing their own investments. For most people, a simple portfolio invested in simple funds is the magic wand of success. Complicated multi-fund portfolios using complicated strategies with complicated funds tends to lend itself to poor execution—if executed at all. Especially when do-it-yourself’ing, it’s important to stay easy.

Pros:

Cheaper. You don’t have to pay a financial planner or investment manager to invest these assets.

Control. You manage the whole account and everything inside.

Empowerment. After you learn how to invest on your own, you can teach friends and family as well.

Cons:

Time. Investing, building, and monitoring a portfolio requires research, which can consume a lot of time.

Expertise. Without a proper understanding of what you’re doing, you do risk making mistakes.

Execution. With all the decisions in your hands, procrastination is easily met without accountability.

So, how do you invest in ESG on your own? There are two things to keep in mind: what are you investing in and where. What you invest in encompasses ideas such as, “what do you want to support” and “what is your ideal allocation.” Meanwhile, where you invest takes into account what custodian you’ll choose to house your capital.

You’ll want to decide what your allocation of equities and bonds will look like first. This is not very straightforward and should look at your age, goals, and cashflow. As a good rule of thumb, the younger you are and the longer your time horizon (and with healthy expected cashflow) generally means you can tolerate a higher allocation to equities. And vice versa. Then you can start deciding what ESG funds you’ll invest in. These can be ETFs, mutual funds, or individual companies, but when evaluating ETFs and mutual funds, consider what strategy the fund uses for its construction. Keep in mind: you’ll want domestic, international, and emerging markets as part of this portfolio for complete equity diversification. As a good rule of thumb for equity allocation, the world market is a good example: 63% U.S., 25% international, and 12% emerging markets. Bonds are a bit different, but a short-term and high-quality ESG bond ETF or mutual fund can be simple and effective. In the end, you should have a portfolio with X% of equities (split amongst U.S., international, and emerging markets) and Y% of bonds, equaling 100%.

Once you have this decided, you can determine where you want to invest. This part is easier—all you have to do is choose a custodian. Popular names include Charles Schwab, Fidelity, and Robinhood, but other institutions can be perfectly fine options. To help evaluate these options, review their costs and fees, account minimums, and investment options. A good brokerage will, along with having SIPC insurance, have no commissions, no minimums, and a very broad list of investment options.

ESG investing with a robo-advisor

Yes, this is a real term. No, it does not mean the Terminator in a suit is managing your investments. But it does mean your portfolio can be managed by zeros and ones, and AI, at a relatively low cost without you doing all the work. Over the years, robo-advisory platforms have undulated in popularity. While the once-expected-adoption-tsunami by investors hasn’t exactly panned out, this is a great method for some investors.

Pros:

Easy. Robo-advisors make investing easier by removing building and monitoring (essentially) from your plate.

Taxes. Some platforms offer tax-smart features like tax loss harvesting and asset location.

Automatic. You can set up automatic investments from your bank straight into your model portfolio.

Cons:

Fees. Seldom is this service free, with average fees hovering 0.25-0.50% annually of assets under management.

Control. Most platforms have models you can pick from but cannot edit, limiting investment choice control.

Necessity. The bells and whistles you pay for, like tax loss harvesting, might not be worth it depending on asset size.

While you’re deciding which robo-advisory platform to engage with, evaluate fees, account minimums, features, and investment options. Most of the time, fees will be based on how much money you invest with that platform, aka assets under management (AUM). The fee will usually be around 0.25-0.50% of those assets annually. While most platforms don’t have an investment minimum, be sure to double check. If you don’t meet their minimum then you can’t use their services. As for features, you’ll want to make sure the account will automatically rebalance, allocate your funds, and maybe even provide tax-smart features like tax loss harvesting and asset location. Lastly, make sure the ESG funds you align with are offered in the model portfolio options. These platforms can be very limited in options.

Once you’ve decided on the robo-advisor platform, the rest is quite streamlined. The robo-advisor will walk you through how to invest, connect accounts, and monitor for progress. Especially when contributions can be automated, the rest is very easy. Just check back in every so often to make sure the platform is running as it should.

ESG investing with a financial planner

A financial planner is a conductor of individual and familial financial pictures. As an orchestra director leads performances, sets tempos, and interprets the music, a financial planner will guide you through your financial strengths and weaknesses, keep you on track, and simplify your finances. As a piece of this relationship, financial planners can also assist with aligning your investments and values—also known as ESG investing.

Pros:

Personal. A financial planner can personalize your ESG investments in line with your goals, needs, and wants.

Comprehensive. ESG investing is just a piece of the comprehensive picture you and the planner will work on.

Expertise. You’ll have peace of mind your investments are designed optimally for your picture.

Cons:

Price. Costs vary between financial planners, but it will most likely cost more than DIY or robo-advisors.

Necessity. Depending on your stage of life, a financial planning relationship might be more than you need.

Generalization. Not all financial planners understand ESG investing and how to incorporate it into practice.

Finding the right financial planner for your specific wants and needs can prove difficult. Fee structures, service options, and specializations differ widely from one planner to the next. To help point you in the right direction, below is a brief description of these differences and how you’ll see them in the wild.

Fee structures:

Fee-based — This structure is a combination of commissions and fees. Commissions introduce conflicts of interests with people recommending you things they are paid to recommend. Avoid this one.

Fee-only — This structure encompasses different, more nuanced fee models. But each one of them eliminates commissions and only charges a fee.

Flat-fee — Charges a set fee not based on hours worked or assets managed. Usually for one-time projects or recurring payments.

Hourly — Charges a fee based on how many hours worked. This varies and is usually based on complexity of your financial case.

AUM fee — Charges a percentage fee based on the amount of assets you let the planner manage. Usually around 1% per year.

Service options:

Advice-only financial planning— This option focuses on financial advice and planning without investment management. If you want to manage your own assets and not pay someone else to do that, this is best for you.

Financial planning and investment management — This options provides investment management alongside financial advice and planning. For those who’d rather pay someone to manage their assets, this is best for you.

Specializations:

Generalist — Some financial planners don’t specialize in any given nuance, like ESG investing. These planners are great for receiving advice until the advice becomes niched.

Specialist — Some financial planners are passionate about certain topics and learn more about it than general information. These planners are especially helpful when your wants and needs become more specific. When researching, as Google or your AI to help find planners specializing in ESG. The planner’s website should also communicate this.

After researching and interviewing financial planners to find one who resonates with you, they’ll guide you through ESG investing. When done correctly, they’ll listen to your values, needs, and goals and provide you with a plan designed for and with you. In the end, you should have a values-aligned plan designed to accomplish your short-, medium-, and long-term goals with taxes, cashflow, investments, insurance, and estate in mind.

Disclosures:

Just Advising LLC is a Registered Investment Adviser in the state of North Carolina. Advisory services are only offered to clients or prospective clients where Just Advising LLC and its representatives are properly registered or exempt from registration. Justin Horowitz is an investment adviser representative of Just Advising LLC. The firm is a registered investment adviser and only conducts business in jurisdictions where it is properly registered, or is excluded or exempted from registration requirements. Registration as an investment adviser is not an endorsement of the firm by securities regulators and does not mean the adviser has achieved a specific level of skill or ability.

Content is for educational purposes only and does not constitute a solicitation or offer to buy/sell any securities or provide personalized investment advice. Past performance is no guarantee of future results. All investments involve risk, including the loss of principal. “Likes” should not be considered a positive reflection of the investment advisory services offered by Just Advising LLC. "Likes," "Shares," or "Comments" are not endorsements of any individual or service. Just Advising LLC is not responsible for the content or accuracy of third-party websites linked herein. Comments are monitored but should not be considered testimonials.

The information presented on this post is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Comments should not be construed as an offer to buy or sell, or a solicitation of an offer to buy or sell the investments mentioned. A professional adviser should be consulted before implementing any of the strategies discussed. Investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for a client's portfolio. All investment strategies can result in profit or loss.

Environmental, Social, and Governance (ESG) investing is qualitative and subjective by nature. There is no guarantee that the criteria used or the investments selected will reflect the beliefs or values of any particular investor. ESG strategies may limit the types and number of investment opportunities available, which could cause a portfolio to underperform the broader market or other strategies that do not utilize ESG criteria. Past performance of ESG-related investments is not an indicator of future results, and there is no assurance that an ESG-oriented approach will result in better performance or lower risk.